|

|

||||||

|

|

Home| Journals | Statistical Calculator | About Us | Contact Us | |||||

|

||||||

| About this Journal | Table of Contents | ||||||

|

|

[Abstract] [PDF] [HTML] [Linked References] International Journal of Statistika and Mathematika, ISSN:, Volume 1, Issue 1, 2011 pp 08-15

Methodologies for Prediction of Stock Market: An Artificial Neural Network

R.K. Dase 1 , D. D. Pawar 2 and D.S. Daspute3 1Assistant professor, MGM�s Medical College, Aurangabad (M.S.), India. 2 Associate professor in Statistics, NES Science College, Nanded (M.S.), India. 3Assistant professor MIMSR Medical College ,Latur(M.S.),India

Corresponding Adresses: Email;- [email protected], [email protected] , [email protected]

Research Article

Abstract: Peoples tend to invest in stocks because of its high returns over time. Stock markets are affected by many highly interrelated economic, social, political and even psychological factors, and these factors interact with each other in a very complicated manner. Therefore it is generally challenging task to predict the movement of stock market. It is observed that conventional statistical techniques for prediction have reached their limitation in applications with nonlinearities in the data set. Artificial Neural Network, a computing system containing many simple nonlinear computing units as neurons interconnected by links, is a well-tested method for financial analysis on the stock market. This paper explains in detail various prediction methodologies for stock market and found that Artificial Neural network could be useful for stock market prediction.

Key words: Artificial Neural Network, Stock market, Time series analysis etc.

1. Introduction:

There are several motivations for trying to predict stock market prices. The most basic of these is financial gain. Any system that can consistently pick winners and losers in the dynamic market place would make the owner of the system very wealthy. Thus, many individuals including researchers, investment professionals, and average investors are continually looking for this superior system which will yield them high returns. The prediction of stock market is without doubt an interesting task. In the literature there are a number of methods applied to accomplish this task. These methods use various approaches, ranging from highly informal ways (e.g. the study of a chart with the fluctuation of the market) to more formal ways (e.g. linear or non-linear regressions).

Analytical Methods (Technical & fundamental) ,Traditional Time Series Prediction Methods,Choas theory ,computer techniques, comparative methods & Machine learning method (i.e Neural Network) these techniques were used for prediction of stock markets. What is common to these techniques is that they are used to predict and thus benefit from the market�s future behavior. None of them has proved to be the consistently correct prediction tool that the investor would like to have. Furthermore many analysts question the usefulness of many of these prediction techniques.

Neural networks are used to predict stock market prices because they are able to learn nonlinear mappings between inputs and outputs. Contrary to the EMH, several researchers claim the stock market and other complex systems exhibit chaos. Chaos is a nonlinear deterministic process which only appears random because it cannot be easily expressed. With the neural networks� ability to learn nonlinear, chaotic systems, it may be possible to outperform traditional analysis and other computer-based methods [5]. In addition to stock market prediction, neural networks have been trained to perform a variety of financial related tasks. There are experimental and commercial systems used for tracking commodity markets and futures, foreign exchange trading, financial planning, company stability, and bankruptcy prediction. Banks use neural networks to scan credit and loan applications to estimate bankruptcy probabilities, while money managers can use neural networks to plan and construct profitable portfolios in real-time. As the application of neural networks in the financial area is so vast, this paper will focus on stock market prediction. Finally, although neural networks are used primarily as an application tool in the financial environment, several research improvements have been made during their implementation. Notable improvements in network design and training and the application of theoretical techniques are demonstrated by the examination of several example systems [5].

2.Analytical Methods:

Before the age of computers, people traded stocks and commodities primarily on intuition. As the level of investing and trading grew, people searched for tools and methods that would increase their gains while minimizing their risk. Statistics, technical analysis, fundamental analysis, and linear regression are all used to attempt to predict and benefit from the market�s direction. None of these techniques has proven to be the consistently correct prediction tool that is desired, and many analysts argue about the usefulness of many of the approaches. However, these methods are presented as they are commonly used in practice and represent a base-level standard for which neural networks should outperform. Also, many of these techniques are used to preprocess raw data inputs, and their results are fed into neural networks as input.

2.1 Technical Analysis:

�Technical analysis is the method of predicting the appropriate time to buy or sell a stock used by those believing in the castles-in-the-air view of stock pricing� [10]. The idea behind technical analysis is that share prices move in trends dictated by the constantly changing attributes of investors in response to different forces. Using technical data such as price, volume, highest and lowest prices per trading period the technical analyst uses charts to predict future stock movements. Price charts are used to detect trends; these trends are assumed to be based on supply and demand issues which often have cyclical or noticeable patterns. From the study of these charts trading rules are extracted and used in the market environment. The technical analysts are known as a�chartists�. Most chartists believe that the market is only 10 percent logical and 90 percent psychological [10]. The chartist�s belief is that a careful study of what the other investors are doing will shed light on what the crowed is likely to do in the future. This is a very popular approach used to predict the market, which has been heavily criticized. The major point of criticism is that the extraction of trading rules from the study of charts is highly subjective therefore different analysts might extract different trading rules by studying the same charts.Some technical indicator categories include filter indicators, momentum indicators, trend line analysis, cycle theory, volume indicators, wave analysis, and pattern analysis. Indicators may provide short or long term information, help identify trends or cycles in the market, or indicate the strength of the stock price using support and resistance levels.An example of a technical indicator is the moving average. The moving average averages stock prices over a given length of time allowing trends to be more visible. Several trading rules have been developed which pertain to the moving average. For example, "when a closing price moves above a moving average a buy signal is generated."[3]. unfortunately, these indicators often give false signals and lag the market. That is, since a moving average is a past estimate, a technical trader often misses a lot of the potential in the stock movement before the appropriate trading signal is generated. Thus, although technical analysis may yield insights into the market, its highly subjective nature and inherent time delay does not make it ideal for the fast, dynamic trading markets of today.

2.2 Fundamental Analysis:

Fundamental analysis is the technique of applying the tenets of the firm foundation theory to the selection of individual stocks�[10]. The analysts that use this method of prediction use fundamental data in order to have a clear picture of the firm (industry or market) they will choose to invest on. They are aiming to compute the �real� value of the asset that they will invest in and they determine this value by studying variables such as the growth, the dividend payout, the interest rates, the risk of investment, the sales level, the tax rates an so on. Their objective is to calculate the intrinsic value of an asset (e.g. of a stock). Since they do so they apply a simple trading rule. If the intrinsic value of the asset is higher than the value it holds in the market, invest in it. If not, consider it a bad investment and avoid it. The fundamental analysts believe that the market is defined 90 percent by logical and 10 percent by physiological factors. This type of analysis is not possible to fit in the objectives of our study. The reason for this is that the data it uses in order to determine the intrinsic value of an asset does not change on daily basis. Therefore fundamental analysis is helpful for predicting the market only in a long-term basis.

The advantages of fundamental analysis are its systematic approach and its ability to predict changes before they show up on the charts. Companies are compared with one another, and their growth prospects are related to the current economic environment. This allows the investor to become more familiar with the company. Unfortunately, it becomes harder to formalize all this knowledge for purposes of automation (with a neural network for example), and interpretation of this knowledge may be subjective. Also, it is hard to time the market using fundamental analysis. Although the outstanding information may warrant stock movement, the actual movement may be delayed due to unknown factors or until the rest of the market interprets the information in the same way. However, fundamental analysis is a superior method for long-term stability and growth. Basically, fundamental analysis assumes investors are 90% logical, examining their investments in detail, whereas technical analysis assumes investors are 90% psychological, reacting to changes in the market environment in predictable ways.

3. Traditional Time Series Forecasting

The Traditional Time Series Prediction analyzes historic data and attempts to approximate future values of a time series as a linear combination of these historic data. In econometrics there are two basic types of time series forecasting: univariate (simple regression) and multivariate (multivariate regression) [9].These types of regression models are the most common tools used in econometrics to predict time series. The way they are applied in practice is that firstly a set of factors that influence (or more specific is assumed that influence) the series under prediction is formed. These factors are the explanatory variables xi of the prediction model. Then a mapping between their values xit and the values of the time series yt (y is the to-be explained variable) is done, so that pairs {xit , yt} are formed. These pairs are used to define the importance of each explanatory variable in the formulation of the to-be explained variable. In other words the linear combination of xi that approximates in an optimum way y is defined. Univariate models are based on one explanatory variable (I=1) while multivariate models use more than one variable (I>1). Regression models have been used to predict stock market time series. A good example of the use of multivariate regression is the work of Pesaran and Timmermann (1994) [15].

4 .The Efficient Market Hypothesis:

The Efficient Market Hypothesis (EMH) states that at any time, the price of a share fully captures all known information about the share. Since all known information is used optimally by market participants, price variations are random, as new information occurs randomly. Thus, share prices perform a "random walk", and it is not possible for an investor to beat the market Despite its rather strong statement that appears to be untrue in practice, there has been inconclusive evidence in rejecting the EMH. Different studies have concluded to accept or reject the EMH. Many of these studies used neural networks to justify their claims. However, since a neural network is only as good as it has been trained to be, it is hard to argue for acceptance or rejection of the hypothesis based solely on neural network performance. In practice, stock market crashes, such as the market crash in October 1987, contradict the EMH because they are not based on randomly occurring information, but arise in times of overwhelming investor fear. The EMH is important because it contradicts all other forms of analysis. If it is impossible to beat the market, then technical, fundamental, or time series analysis should lead to no better performance than random guessing. The fact that many market participants can consistently beat the market is an indication that the EMH may not be true in practice. The EMH may be true in the ideal world with equal information distribution, but today�s markets contain several privileged players who can outperform the market by using inside information or other means.

5 .Chaos Theory:

A relatively new approach to modeling nonlinear dynamic systems like the stock market is chaos theory. Chaos theory analyzes a process under the assumption that part of the process is deterministic and part of the process is random. Chaos is a nonlinear process which appears to be random. Various theoretical tests have been developed to test if a system is chaotic (has chaos in its time series). Chaos theory is an attempt to show that order does exist in apparent randomness. By implying that the stock market is chaotic and not simply random, chaos theory contradicts the EMH .In essence, a chaotic system is a combination of a deterministic and a random process. The deterministic process can be characterized using regression fitting, while the random process can be characterized by statistical parameters of a distribution function. Thus, using only deterministic or statistical techniques will not fully capture the nature of a chaotic system. A neural networks ability to capture both deterministic and random features makes it ideal for modeling chaotic systems.

6. Other Computer Techniques:

Many other computer based techniques have been employed to forecast the stock market. They range from charting programs to sophisticated expert systems. Fuzzy logic has also been used.

Expert systems process knowledge sequentially and formulate it into rules. They can be used to formulate trading rules based on technical indicators. In this capacity, expert systems can be used in conjunction with neural networks to predict the market. In such a combined system, the neural network can perform its prediction, while the expert system could validate the prediction based on its well-known trading rules. The advantage of expert systems is that they can explain how they derive their results. With neural networks, it is difficult to analyze the importance of input data and how the network derived its results. However, neural networks are faster because they execute in parallel and are more faults tolerant. The major problem with applying expert systems to the stock market is the difficultly in formulating Knowledge of the markets because we ourselves do not completely understand them. Neural networks have an advantage over expert systems because they can extract rules without having them explicitly formalized. In a highly chaotic and only partially understood environment, such as the stock market, this is an important factor. It is hard to extract information from experts and formalize it in a way usable by expert systems. Expert systems are only good within their domain of knowledge and do not work well when there is missing or incomplete information. Neural networks handle dynamic data better and can generalize and make "educated guesses." Thus, neural networks are more suited to the stock market environment than expert systems.

7. Comparing the various models:

In the wide variety of different modeling techniques presented so far, every technique has its own set of supporters and detractors and vastly differing benefits and shortcomings. The common goal in all the methods is predicting future market movements from past information. The assumptions made by each method dictate its performance and its application to the markets. The EMH assumes that fully disseminated information results in an unpredictable random market. Thus, no analysis technique can consistently beat the market as others will use it, and its gains will be nullified. I believe that the EMH has some merit theoretically, but in real-world applications, it is painfully obvious that there is an uneven playing field. Some market participants have more information or tools which allow them to beat the market or even manipulate it. Thus, stock market prices are not simply a random walk, but are derived from a dynamic system with complexities to vast to be fully accounted for. If an investor does not believe in the EMH, the other models offers variety of possibilities. Technical analysis assumes history repeats itself and noticeable patterns can be discerned in investor behavior by examining charts. Fundamental analysis helps the long-term investor measure intrinsic value of shares and their future direction by assuming investors make rational investment decisions. Statistical and regression techniques attempt to formulate past behavior in recurrent equations to predict future values. Finally, chaos theory states that the apparent randomness of the market is just nonlinear dynamics too complex to be fully understood. So what model is the right one? There is no right model. Each model has its own benefits and Short comings. I feel that the market is a chaotic system. It may be predictable at times, while at other times it appears totally random. The reason for this is that human beings are neither totally predictable nor totally random. Although it is nearly impossible to determine a person�s reaction to information or situations, there are always some basic trends in behavior as well as some random elements. The market is a collection of millions of people acting in a chaotic manner. It is as impossible to predict the behavior of a million people as it is to predict the behavior of one person. Investors are neither mostly psychological as predicted by technical analysis, nor logical as predicted by fundamental analysis. Our approach and view on the world varies daily in a manner that we do not even fully understand, so it follows that the stock market behaves in similar ways. In conclusion, these methods work best when employed together. The major benefit of using a neural network then is for the network to learn how to use these methods in combination effectively, and hopefully learn how the market behaves as a factor of our collective consciousness.

8. Machine Learning Methods:

Several methods for inductive learning have been developed under the common label�Machine Learning�. All these methods use a set of samples to generate an approximation of the underling function that generated the data. The aim is to draw conclusions from these samples in such way that when unseen data are presented to a model it is possible to infer the to-be explained variable from these data. The methods we discuss here are: The Nearest Neighbor and the Neural Networks Techniques. Both of these methods have been applied to market prediction; particularly for Neural Networks there is a rich literature related to the forecast of the market on daily basis.

8.1 Nearest Neighbor Techniques:

The nearest neighbor technique is suitable for classification tasks. It classifies unseen data to bins by using their �distance� from the k bin centroids. The �distance� is usually the Euclidean distance. In the frame of the stock market prediction this method can be applied by creating three (or more) bins. One to classify the samples that indicate that the market will rise. The second to classify the samples that indicate fall and the third for the samples related with no change of the market [16]. Although this approach can be used to predict the market on daily basis we will not attempt to apply it on this study. The main reason is that we will not attempt a classification but a regression task. The classification task has the disadvantage that it flattens the magnitude of the change (rise of fall). On the other hand it has the advantage that as a task it is less noisy comparing to regression. Our intention is to see how well a regression task can perform on the prediction of the market.

9.2 Applications of Neural Networks to Market Prediction:

9. 2.1 .Introduction:

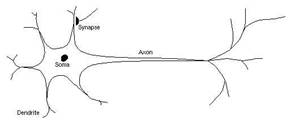

The ability of neural networks to discover nonlinear relationships in input data makes them ideal for modeling nonlinear dynamic systems such as the stock market. Various neural network configurations have been developed to model the stock market. Commonly, these systems are created in order to determine the validity of the EMH or to compare them with statistical methods such as regression. �A neural network may be considered as a data processing technique that maps, or relates, some type of input stream of information to an output stream of data� [2]. Neural Networks (NNs) can be used to perform classification and regression tasks. More specifically it has been proved by Cybenko (cited in Mitchel, 1997) that any function can be approximated to arbitrary accuracy by a neural network [11]. NNs are consisted of neurons (or nodes) distributed across layers. The way these neurons are distributed and the way they are linked with each other define the structure of the network. Each of the links between the neurons is characterized by a weight value. A neuron is a processing unit that takes a number of inputs and gives a distinct output. Apart from the number of its inputs it is characterized by a function f known as transfer function. The most commonly used transfer functions are: the hardlimit, the pure linear, the sigmoid and the tansigmoid function. Ample of work is done on Neural Network for predicting stock market by many scientist, as a neural network being most ideal technique for predicting stock market putforth by some researcher is enlighted as below. Research of Kimoto, T., Asakawa, K., Yoda, M. and Takeoka, M [7] (1990) seems to be the first research where a system based on neural networks has been tried in a real environment (Tokyo Stock Exchange Prices Indexes) and has succeeded in beating the market. They use five inputs; vector curve, turnover, interest rate, foreign exchange rate and Dow Jones average index. The approach followed is the modular network approach, in which different networks learn for different data items. Each expert module has its own input domain and preprocessing unit. A final post-processing unit has combined the results to an overall output. The research has been further funded by an investment firm. Each modular network has one hidden layer, uses standard sigmoid as an output function and is trained using back propagation algorithm. Jing Tao YAO & Chew Lim TAN [6] in 1998 showed neural networks are suitable for financial forecasting and marketing analysis .they can be very much useful for financial time series, such as stock exchange indices etc. and they shows that NN models can outperform conventional models in most cases. Benjamin W.Wah & Minglun Qian [3] in 2002 developed a new constrained artificial neural network (ANN) formulation and learning algorithms to predict future stock prices, a difficult time series prediction problem. Their experimental results demonstrate good prediction accuracy in a 10-day horizon. They used recurrent neural network. Erdinc Altay and M. Hakan Satman ESQ [4] in 2005,studied the Istanbul Stock exchange can be forecasted through the learning procedure of Artificial Neural Network and compared the forecasting performance of artificial neural network with linear regression and buy and hold strategies� Qing Cao, Karyl B Leggio, Marc J.Schniederjans [12] in 2005 used Artificial Neural Networks to predict stock price movement (i.e. price return ) for firms traded on the Shanghai Stock Exchange and compared the predictive power of univariate and multivariate neural network models and results shows that Neural Network outperform the linear models compared and these results are statistically significant across our sample firms and indicated neural networks are useful tool for stock price Prediction in emerging markets like china. AkinwaJe, A.T., IbharaJu, F.T. and Arogundade,[1] in 2006. Artificial neural network was used to predict movements in stock prices in Nigerian Stock Exchange market. Studies were carried out for the prediction of stock index values as well as daily direction of changes in the index. A network was designed using Back Propagation Algorithm (BPA) to predict stock index values and prices in the exchange for a period of 90 days. The data collected during this period was processed using the BPA algorithm to get an output such that the error between the actual indices and prices, and the computed output was brought to minimum. About 90% of the data was used for the actual training while the remaining 10% was used as test data. The same data was also processed using the Least Squares (LS) method. The results show that BPA algorithm has superior performances in terms of the accuracy of prediction over the LS method. This result of the study is useful to stock market operators. Qing Cao ,Mark E.Parry and Karyl B. Leggio [13] in 2009 examined the predictive ability of several well-established forecasting models, including dynamic versions of a single factor CAPM �based model and Fema and French�s three-factor model , compared these models with artificial neural network(ANN) models that contains the same predictor variables but relaxes the assumptions of model linearity. And find no statistical difference in the forecasting accuracy of CAPM and three factor model and also found that neural networks may be a useful tool for stock price prediction in emerging markets. Roza Gharoie Ahangar , Mahmood yahyazadehfar & Hassan Pournaghshband [14] in 2010 estimated the stock prices of activated companies in Tehran (Iran) stock Exchange. It is used Linear Regression and Artificial Neural Methods and compared these two methods. And presented an equation for two methods and compared their results which shown that artificial neural method is more efficient than linear regression method. 9. 2.2 Biological Neuron: - Much is still unknown about how the brain trains itself to process information, so theories abound. Biological brains are composed of cells called neurons. Each neuron has cell body or Soma. From which extended a single axon (The neuron sends out spikes of electrical activity through a long, thin stand known as an axon), along which impulses are transmitted to other neurons when the soma is sufficiently excited by incoming impulses. These incoming impulses are received by sensors called dendrites. The area where the impulses are received is called synapse. Never impulses are transmitted from one neuron to another across synapses. These neural structures operate electro chemically. This means that the brain work on electrical impulses that are created by chemical action. When the combined interplay of many incoming impulses reaches a level of excitement or electrical charge called as threshold.[5] Synapse converts the activity from the axon into electrical effects that inhibit or excite activity from the axon into electrical effects that inhibit or excite activity in the connected neurons. Electrical activity down its axon. Learning occurs by changing the effectiveness of the synapses so that the influence of one neuron on another changes.

9. 2.3 The Mathematical Model:- An appropriate notational convention, regression model in which the expected response, y, is related to the values of x = (x1��.� xp) of covariance according to,

Y = wo

+ The notational convention is that the circle represents a computational unit, into which the xj� s are fed and multiplied by the respective wj�s .The resulting products are added and then a further wo is added to provide the eventual output [5] . In this way we create a neural network representation of a very familiar statistical construct, because figure 1 is a version of a standard neural network called the simple or single �unit perceptron.

10. Conclusion:

Prediction of stock market not an essay task. Scientist try to develope such a methodology that investors, brokers could get maximum profits. At earliest investors would use different methodologies like Time series Analysis, Fundamental Analysis ,Technical anaysis.After that Efficient market hypothesis,choas theory, Some comparing models, various computer techniques were used. In contemporary period ,Neural Network methodology is very effective for predicting stock markets.

11. References:

[1] AkinwaJe, A.T., IbharaJu, F.T. and Arogundade �Comparative analysis of artificial neural network�s Back propagation Algorithm to Statistical Least Square method in security prediction using Nigerian Stock Exchange Market.� Proceedings of Second Conference of Science & National Development, pp10-16, oct 2006 [2] Azoff E. M. Neural network time series forecasting of financial markets.Chichester: John Wiley and Sons.1994. [3] Benjamin W.Wah & Minglun Qian � Constrained Formulation and algorithms for stock price prediction using Recurrent FIR Neural Networks�, prof.National Conferences on Artificial Intelligence , AAAI,2002. [4] Erdinc Altay and M. Hakan Satman � Stock market forecasting; Artificial Neural Network and linear regression comparison in an emerging market� Journal of financial management and analysis ,vol. 18(2),pp.18-33,2005. [5] Haykin S. �Neural Network: A Comprehensive Foundation�, Macmillan College Publication, New York, 1994. [6] Jing Tao YAO & Chew Lim TAN � Guidelines for Financial Forecasting with Neural network�,jounal of forecasting�,, Proceedings of International Conference on Neural Information Processing, Shanghai, China, 14-18 November, pp757-761,2001 [7] Kimoto, T., Asakawa, K., Yoda, M. and Takeoka, M.� Stock market Prediction systemwith modular neural networks�, In Proceedings of IJCNN-90, San Diego, 1990. [8] Kunwar Singh Vaisla and Authosh kumar Bhaatt,�An Analysis of performance of Artificial Neural Network technique for stock market forecasting�, International Journal on Computer Science and Engineering Vol. 02, No. 06, pp2104-2109, 2010. [9] Maddala G.S. Introduction to econometrics. New York, Toronto: Macmillan Publishing Company,1992. [10] Malkei B. G..). A random walk down wall street. New York, London: W. W. Norton & Company, 7th ed, 1999 [11] Mitchell M.T. Machine learning. New York: The McGraw-Hill Companies,1997. [12] Quig Cao,Kary B.Leggio and Marc J.Schniederjans � A Comparison between Fema and French�s model and artificial neural networks in predicting the Chinese stock market�, Computers and operation Research,vol .32 ,pp2499-2512,2005. [13] Qing Cao, Mark E.Parry and Karyl B.Leggio �The three-factor model and artificial neural networks; predicting stock price movement in china�, Springer science and business Media vol.250, 2009. [14] Roza Gharoie Ahangar,Mahmood yahyazadehfar & Hassan Pournaghshband,� The comparison of methods Artificial Neural Network with linear regression using specific variables for prediction stock prices in Tehran stock Exchange�, International journal of computer science and Information Security ,vol.7,no.2, pp38-46, Feb 2010. [15] Pesaran H. M. & Timmermann A. Forecasting stock returns: An examination of stock market trading in the presence of transaction costs. Journal of Forecasting, Vol. 13, pp 335-367,1994. [16] Yuehui Chen, Bo Yang and Ajith Abraham,�Flexiable Neural Trees ensemble for Stock index modeling� Neurocomputing, vol.70, pp 697-703, 2007

|

|||||

|

||||||